This is a post from Peter Nunns. See Part 1 here.

In my previous post I gave an overview of the postgraduate research project I’ve been working on over the past year. It looks at the causes and economic consequences of rising regional housing prices in New Zealand.

Nobody reading this will be surprised to hear that house prices and rents have been rising much faster than wages over the last generation, and that Auckland has experienced some of the most rapid increases.

But I think that most people would have trouble explaining exactly why prices have increased so much. At the macroeconomic level, there are many potential causes: the growth of the financial sector and the increasing availability of cheap credit, tax policies that incentivise home-buying, a fast-growing population, and a variety of barriers to building more homes. A 2011 research paper from three OECD researchers summed this up nicely.

However, macroeconomic factors don’t necessarily explain why prices have risen more in some places relative to others. For instance, if banks are lending more freely, it should push up prices in Dunedin and Auckland to a similar degree. That hasn’t been the case, so we need to take a look at what’s going on at a microeconomic level.

If a house that was bought in, say, 2005 sells for a higher price in 2015, there are a couple of things that might have caused the increase.

First, the owner may have renovated the house or built an addition onto it. Investing in the property to make it nicer will increase its value.

Second, demand to live in that location might have increased. This could reflect changing preferences for different places, improvements to the quality of schools, shops, and public spaces in the area, or changes to transport accessibility, eg due to a new rapid transit route.

Third, the city may not have enough housing to keep up with demand. Scarcity can drive up prices even for crummy houses in bad locations, as people grow increasingly desperate for somewhere to live.

All three factors are at work in Auckland, and elsewhere in New Zealand. So I used a method developed by economists Ed Glaeser and Joseph Gyourko in a 2003 paper to identify how much of an impact each of these factors has had over the last generation.

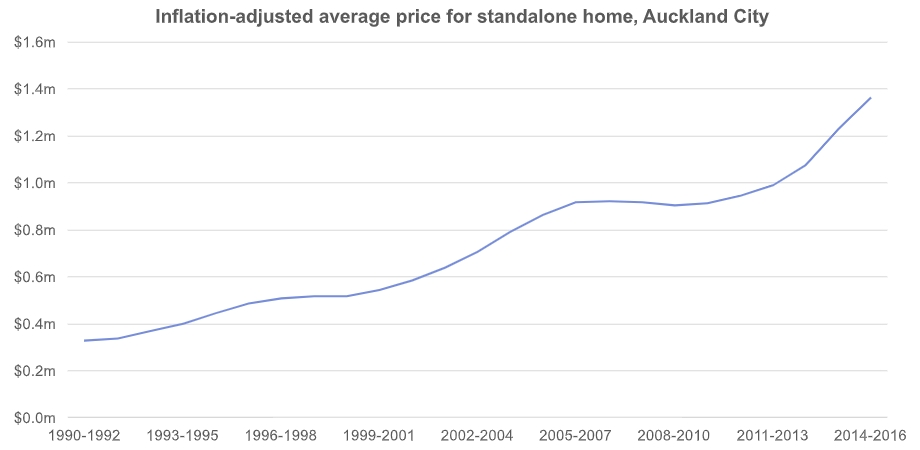

The following chart shows the rise in the inflation-adjusted price for an average standalone house in the former Auckland City Council area, over the last generation. (I’ve focused on standalone houses as Glaeser and Gyourko’s statistical methods are easiest to apply to house sales, but the same basic dynamics apply to apartments as well.) In 1990-1992, the average house sold for around $330,000. By 2014-2016, prices had risen to over $1,360,000 – a fourfold increase.

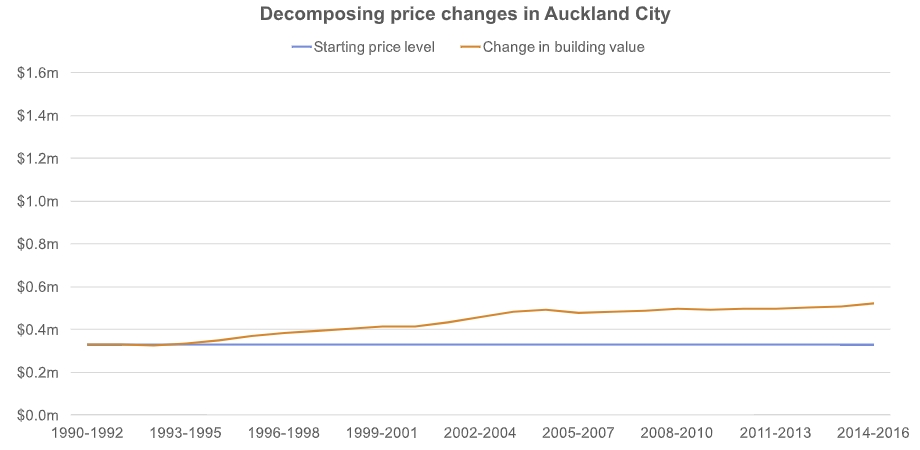

The orange line in the following chart shows how much of this increase can be explained by building improvements and renovations. To calculate this, I used data from three-yearly ratings valuations, which assess the value of buildings on each site. This shows that, if section prices had held constant but homeowners had continued to invest in renovations, then average prices would have only risen to $520,000.

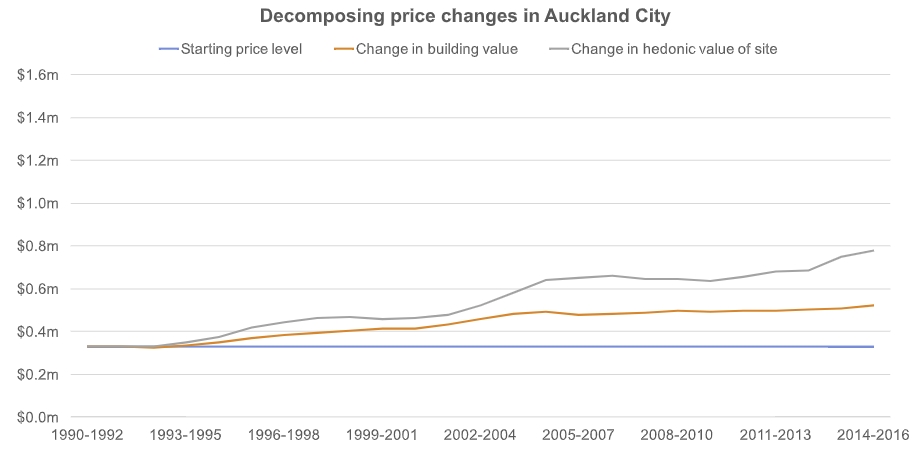

Next, I looked at the role of increasing demand for residential land in different places. To do so, I ran 1800 regressions – one for each council area over each of the 25 time periods in the analysis – and used the results to estimate the ‘hedonic’ value of land. In effect, I compared what buyers are actually willing to pay for a slightly smaller or larger residential site.

This analysis indicates that the underlying demand for residential land has increased in Auckland, reflecting growth in incomes, increasing preferences to live in cities, and improving urban amenities. If we also take this into account, it suggests that Auckland City house prices should have risen to around $780,000 over this period, as shown by the grey line on the following chart.

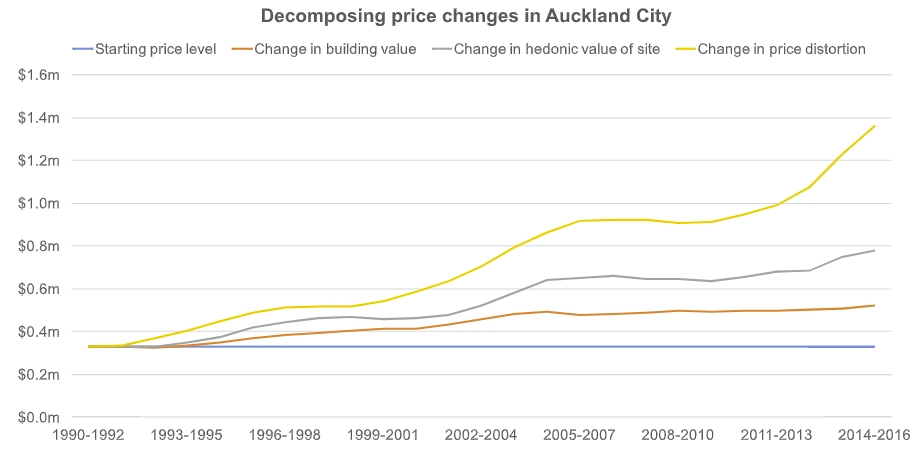

However, $780,000 is a lot less than $1,360,000, which means that increasing scarcity of housing in Auckland has played a large role in rising prices. The final chart suggests that our inability to build enough new housing in the right places has driven more than half of the house price increases that Auckland City has experienced over the last generation.

Finally, it’s important to note that many places have not experienced the same trends as Auckland. For instance, here’s the same chart for Whangarei District, where average house prices rose from around $160,000 to $400,000. Here, the role of improvements to buildings is proportionately larger, and the impact of increasing scarcity of housing is considerably smaller.

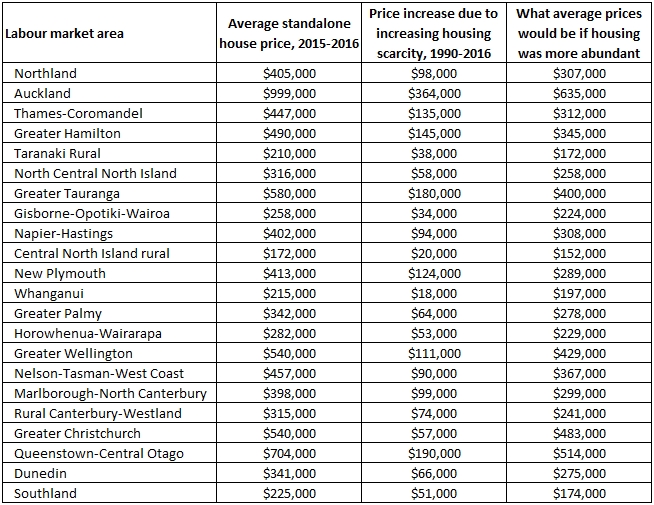

In fact, if you look around, Auckland seems like a major outlier: it has experienced larger scarcity-driven price increases than anywhere else. The following table shows how much of an impact a lack of housing has had on prices in different regions. (I’ve divided NZ into 22 areas that roughly correspond to commuting zones around major cities, plus rural areas.)

Prices in Auckland would be higher than elsewhere in the country even if housing was more abundant – people value living here! – but the gap would be much smaller than it is today.

This naturally leads on to the question of what else would have happened as a result. Would more people live in Auckland? Would fewer live in Whangarei? What impacts would that have on economic productivity?

Next week: Spatial equilibrium!

Processing...

Processing...

It would be interesting to see the data for the regions over the past two years. We know of over a dozen people directly who have moved out of Auckland for quality of life issues, including ourselves. In the Thames Coromandel area the advertised prices have moved up around 25%. in that period. There are now around 400 people commuting to the Auckland area from Thames every day. Areas like Cambridge, Morrinsville, Napier, Hasting and Havelock North have seen similar changes. So there is likely a secondary effect of overflow from Auckland due to the price distortions and other factors. This will make things like regional rapid rail more cost effective or enable companies to relocate to satellite regions as the skilled workforce will already exist outside of Auckland.

Interestingly, I met a nurse recently who had moved from Christchurch to Auckland because:

– it’s warmer

– her grown up children on their OE’s can visit her more easily

– the public transport allows her to live without a car

– she loves our waterfront and cultural events

And presumably because as an experienced nurse, her age didn’t count against her in a city where young nurses find it harder to afford to live.

Bucking the trend, I know but interesting none the less.

I think there’s a lot of potential for regional rapid rail. As you note, spillover to the Waikato is already well underway, and it will work better if a high-quality rail service is available. I can’t comment on the details, but it also seems quite important to have a joined-up approach to spatial planning along any such infrastructure corridor.

I’ve been reflecting a bit on the Copenhagen Finger Plan, which has some interesting principles to reflect on: https://danishbusinessauthority.dk/sites/default/files/fp-eng_31_13052015.pdf

And yes, Heidi – people will move in all directions for all sorts of reasons! I think it is definitely true that Auckland has improved over the last decade, and that will have partly offset the impact of rising house prices.

Whether moving in to or out of Auckland improves your quality of life depends on your priorities. As a civil engineer I moved to Auckland to work on more interesting projects and also for the amenities that a large city offers. I could easily find a job in other parts of NZ but don’t really want to move back to the smaller cities or rural areas.

Thanks Peter. It’s good to see the different factors separated out like this. Where do these factors sit in the analysis:

– Developers building too-big houses so the median house price is for a supply of larger housing than the market wants.

– Developers making money (more money?) from the rezoning of land on the periphery than from the provision of homes on that land?

Bigger houses are less of an issue if material prices are reasonable;

I’d say an equally preposterous situation is a 2x bed apartment costing $750k – $800K.

+1

I think it’s all related. If developers weren’t making money from rezoning but concentrating on making money from the actual provision on new homes, they’d find they’d make more money from apartments than from mansions on the outskirts (going by Mark Todd’s analysis.)

More apartments would reduce their scarcity value. Fewer expensive mansions would bring the median price down.

Developers get good at delivering what the market wants. When there is a shortage of houses they focus on the top end as there is more profit there. Land supply has been constrained, the wealthy bid up the price of land and buy the sections, then they have a big house built. If you want smaller houses as well then the answer is allow more houses to be built. If you want someone to blame then aim it at the anti-sprawl people. They did it. Starting with Phil Warren and the Auckland Growth Strategy numpties.

Yeah dammit, we need more homes in Pokeno NOW!..wait, that’s not actually Auckland, oops wrong blog.

Miffy, the knock-on problems from sprawl are horrendous.

Regional development, with kick starters for local circular economy initiatives and subsidies galore is an option.

Mandated occupancy levels of each home and confiscation of unoccupied multiple residences would be less popular but would free up space and largely only affect the privileged.

Less ideal would be contraceptives in the water supply, sterilisation as a condition of immigration, and culling us once we’re 50. 🙂 (My tongue is in my cheek in case someone out there is in doubt.)

But more sprawl? Freeing up yet more land? That should not be an option. This is a city whose problems stem from being too sprawled out. We’re not able to provide adequate services because of our low density. We’re not able to maintain the strung out infrastructure that we have.

Advocating for more sprawl is madness.

The only rational options that maintain the environment around the city so it can support us with ecological services and food, and doesn’t leave future generations with burdensome infrastructure, are: intensification, and regional development. Take your pick from those.

+100

Heidi how do you feel about electrification to Pukekohe ? Surely this just helps destroy Aucklands most fertile land in houses.

Mike, I’d like to see a strong regional train and bus passenger network, and much more freight taken by rail. I imagine electrification of the rail throughout the north island should be a part of that.

Zoning that land for development is the problem, and unbelievable when you consider the quality of that soil (chemical burden notwithstanding).

“Developers get good at delivering what the market *allows*”

Fixed that for you. My mum lives very near to the new developments at Long Bay. Everytime we go to the café there I overhear people commenting that the houses are huge and unaffordable. Of course they are, the NIMBY group up there managed to get the council/courts to cap the maximum number of dwellings, so Todd built the biggest dwellings they could. If he NIMBYs had capped floor area, then Todd would have maximized the number of dwellings possible in that floor area.

TLDR: developers build big unaffordable homes because NIMBYs don’t let them build lots of homes.

That’s a great – and very insightful – comment Sailor Boy. Hung by their own petard then? 😉

So many factors at play, we have had. **sounds like Yoda**. Restrictions on foreign ownership and speculative investment of big and not actually rented houses will impact on this type of development in my opinion.

No mention of the fact that a huge number of Auckland houses were snapped up by China based investors? This would flow through into the scarcity angle as they increased demand while supply didn’t (and couldn’t keep up).

I hope someone is measuring the effect in NZ of China’s changed tax laws.

“No mention of the fact that a huge number of Auckland houses were snapped up by China based investors?”

That’s actually a huuuuuuge factor on prices. Nothing to do with racism. Its just recognising that a greater pool of available money chasing a fixed number of properties for sale, is going to have an upwards effect on pricing. Fact of life. The losers will always be the local people with average incomes, if the external buyers have above-average incomes, or access to larger pools of money. And China and India, with over a billion people each, are always going to have a disproportionate effect on a pool catering for just under a million Auckland homes.

A similar thing occurred in Croatia, where housing used to be affordable in cities like Dubrovnik and Split. Post Balkan war, and with increased desire for property in warmer climate from Brits and Germans, there has been a massive boom in house prices and the locals are being priced out of the market. It will be interesting to see if prices go down when the Brits force themselves out of Europe, or if the Germans just move in and take up the slack.

There’s an obvious answer therefore: ban foreign ownership. Key’s National government was dead against that, given that incoming migrants brought in money with them and were requested to “invest” it – ie simplest route was to buy property. The money would, in theory at least, then flow on to the general economy – in reality, the sellers of the property tended to then buy another property, and if mortgages were involved, then the money flowed back to the big Ozzie banks. Net result – more money sloshing around on the books, but not a whole lot of real investment.

It is a Pandora’s box – once let out, it can never go back in. Few in Auckland would really want a 50% reduction in house value, which in reality is the only thing that is going to bring house prices anywhere near to their original worth.

Not sure this can really be claimed as fact. I’ve never seen a jot of evidence showing that this is the case or for that matter that it isn’t, it’s pure speculation, which reached it’s nadir with Labour’s ‘Asian sounding names’ debacle.

I’m all for restricting the sale of land to foreigners purely for sovereignty reasons, but I’m not convinced it will reduce house prices, which it should if it is the ‘huge factor’ that you claim.

How about this analogy:

Imagine 30 years ago we had so much meat that eye fillet steak was affordable to the majority of the population. Then imagine over the next 30 years that the demand for eye fillet steak increased due to factors like population increase and internationalisation, and hence the price increased to a point where the majority of people could not afford it. But people didn’t go hungry – they instead ate cheaper cuts of meat, chicken, vegetarian, etc. Then imagine Auckland Council decided that it would appear better if everyone still ate eye fillet – and banned the production of all other foods. Lots of people went hungry – but at least no one had to eat chicken!

Brilliant.

I wonder how much cost of housing impacts on migration to cities. For example, assuming all other variable held equal, using the scenario from the last table where “housing was more abundant”, would the comparatively lower prices, which are indeed significantly lower, would that have ushered in further migration flows, thus meaning housing was in fact not quite so abundant. This would close the gap on supply and demand somewhat…??

Or it could go the other way – migrants may see high house prices as a sign of a good economy and a more attractive place to live.

That’s the topic of the third post!

I look forward to it Peter. I’ve always wondered, you can have a strong urban economy without high housing prices, but can you have high house prices without a strong economy?

Sure. Look at ski resort towns or beachfront retirement and holiday communities. They typically have low wages and poor employment opportunities (except for seasonal workers), but house prices can be high due to the fact that people with ‘outside money’ are buying the lifestyle.

Nelson is a good example. Prices there are similar to Christchurch but with 1/7th of the population. The “Sunshine Wages” are low and the eceonomy is propped up by baby boomers moving from other areas.

Those are fundermental analysis.

There are also human issues such as the “Fear of missing out” when people think the auckland capital gain will never stop during the peak of auckland price.

Yes, I’ve seen that fear drive young people into the housing market despite the level of debt required being unhealthy. I’ve also seen them subsequently argue against the need for prices to come down because it would hurt them directly.

If we can fix the drivers of housing being unaffordable and too far from the city, it would also be good to try to provide more equity between the generations. My generation needs to be taxed more to help the young ones out.

Unfortunately biological clocks don’t tick in line with economic cycles. I am not looking forward to buying in the next 12 months, but I realistically don’t have a choice.

Congratulations, Buttwizard! That’s exciting.

True, but only because we live in a Country where there is no alternate option such as long term rental, share schemes or our willingness to invest our finances in anything other than property.

Although it may be a blessing in disguise. I have three friends living around Europe that are a similar age and skill set to me. They don’t really own anything except perhaps some money in their retirement scheme. Whereas myself and most friends in NZ own a fair chunk of a house.

One problem is, how do you save money long term for retirement. One of the main ways, traditionally, is making sure you don’t pay rent anymore when you’re retired.

I have often heard about “compounding interest”, “start early”, blah, blah. For young people that is pure internet lore. Savings no longer earn interest. That 10 year term deposit barely keeps up with inflation (or not).

This has been so in Europe for over a decade. New Zealand was a bit behind the curve but is now catching up. Savings, term deposits, Kiwisaver, you name it. None of them return a positive real interest rate anymore.

roeland – if you are saving for your retirement as a young person your money shouldn’t be anywhere near a bank, there is still pretty decent compound growth for money in a indexed fund. After 40 years this would cover the rent and a lot more.

Well, yes. I thought Kiwisaver is at least in part backed by those index funds (if you set up the right kind of fund).

Also don’t you already need a big pile of money to meet the “minimum investment” for any of those higher yield funds?

roeland – there are funds available that are exclusively in NZ, Australian or overseas shares that have a minimum outlay of less than $1000, or as you say Kiwisaver growth funds.

Private equity funds that investing in non-listed companies are the ones that tend to have a much higher minimum investment.

When I was studying at Uni (back in early 2000’s), a few lecturer’s commented on that they anticipated housing prices would drop significantly due to a mass amount of baby boomers approaching retirement age and selling all within the next 5-15 years.

This certainly hasn’t happened, and I don’t really see it happening in the near future either.

Swarms of ex-Aucklander’s leaving pushes up prices of land/housing out in the regions too, I think those areas may be more at risk of large drops in prices once retirement age hits the baby boomer generation.

“…they anticipated housing prices would drop significantly…”

Which is precisely the reason that Key et al encouraged the inwards migration of so many new people. It was clear to everybody that there could, in theory, be a glut of houses – so, bring in more people, especially young people, who will earn, pay tax, and fill the coffers for the retirement pensions of Key’s generation. Cynical, but it worked.

While I agree that net migration has helped drive property prices, I’m not sure the previous government ever had much control over it. The biggest impact on net migration was the dramatic fall in New Zealanders heading to Australia due to the Australian downturn, I don’t think anyone predicted this and it certainly wasn’t something Key had any control over.

Yes it’s really just good fortune for the current and previous governments that under each of their watches immigration has done what they’ve wanted it to, because neither of them can really take any credit for it. Cycles do what they will do.

The one other factor which needs to be considered is interest rates.

Mortgage rates were at 15% in 1990 (https://www.elite6.co.nz/finance-insurance/interest-rates-historical-low/) and are now 5 – 6%.

The asset price people can leverage at up to 30% of income (typical mortgage max) is now a lot higher at the lower interest rate.

Did you read the post? Peter covers of macro factors, such as interest rates.

To reiterate, as interest rates are constant across the country they can explain why prices nationally might move up or down, but they can’t explain why prices in Auckland’s increase more than Whangarei, for example.

Agreed, but they are a factor in the total quantum of increase.

Prices would not be “By 2014-2016, prices had risen to over $1,360,000” if interest rates were still 15%

In general, I agree. If mortgages were harder to get / more expensive, then we probably would have also seen less appreciation in the underlying value of land and less investment in renovations and additions. However, it’s not clear to me whether we’d be better off as a result of those changes, whereas I do think that bringing down scarcity-driven price increases would make us better off.

Why not go back to the 1980s when interest rates were above 20 percent.

Peter to what extent does natural geography play a part in higher house prices? It will always be much more expensive to expand housing supply in Wellington because of the natural geography. I believe Auckland has the third largest harbour in the world, that must impose a significant constraint on housing development, at least compared to cities without large harbours (or extinct volcanoes).

I wouldn’t say its expensive to expand housing supply due to natural geography, land prices might go up when there is less land, so it may be more expensive to supply traditional NZ housing of 1 storey bungalows.

Some interesting data I’d like to see is a dwellings per building analysis on Auckland vs Wellington. Would be interesting to see if Welly had more Townhouses and Apartments per capita than Auckland.

The Unitary Plan is supposed to supply us with enough land, or close to what we need, yet we are consenting and building way way below what is available despite people on here and National trying to free up more Greenfield to line their pockets. Material costs, construction labour shortage, council consenting process and costs are really holding back the sector.

I think it does play a role. Exploratory analysis in an appendix to the thesis suggests that places with more geographic constraints tend to end up with larger house price distortions, indicating greater scarcity of housing relative to demand. But it’s unclear to me whether this is a causal effect, and if so, how the chain of causation works.

Geographic constraints often coincide with better natural amenities – Auckland is more scenic than Hamilton in part because it’s got harbours and beaches. All else equal, people are willing to pay higher prices to live in scenic places.

People living in more scenic places may also demand more zoning rules to preserve natural landscapes – think Auckland’s volcanic cone view protections. This is an additional channel through which geographic constraints can slow down home-building. Here’s a great paper from the US that investigates these issues: http://www.brown.edu/Departments/Economics/Faculty/Matthew_Turner/ec2410/readings/Saiz_QJE_2010.pdf

Agree, Queenstown is probably the best example in New Zealand of zoning rules severely restricting the supply of housing.

Thanks Peter for a very interesting analysis. Not sure if you have seen it but there was an interesting article published on LinkedIn where an Australian economist looked at the house price trend in Melbourne. He highlighted several similar factors, and also pointed out how availability of greenfield lots for housing development at the fringe was NOT the main cause of the problem. In both cases, constraints on inner urban up-zoning appear a likely cause.

https://www.linkedin.com/pulse/housing-affordability-crunch-how-did-melbourne-get-giannakodakis/

Thanks. Good link to have. This myth needs busting fast to get public and politicians away from feeling that reality puts them between and rock and hard place. It doesn’t.

Good article. Auckland would exhibit some similar trends, but I don’t think they’d be quite as pronounced.

One point I’d add is that, looking at things on the ground, construction costs are going to be the big barrier to intensification over the next few years, rather than zoning per se. This is going to make it more challenging to overcome housing scarcity than previously assumed.

Thanks Peter. A very good article – the work that underlies your graphs must have been heavy.

Thanks Bob! 1800 regression models! Actually, multiples of that once you factor in a couple of model specification tests I also ran. Fortunately, it’s possible to automate that process 😉

what do you economists think would happen if they capped house pricing in Auckland? the economy is unstable already because of the inflation around house prices….? it’s my parent’s generation and foreign investment that is going to continue to get the cream of housing prices. while the younger generations struggle to push through forever? how will the government combat this? or are we all going to end up moving to bumfuck nowhere so we don’t have to live in the grime that is Auckland/ ORKland- (obviously due to all the meth users that run the workforce). The crime rate makes Auckland seem like America already, this is all driven by the cost of living don’t you think?. Who’s sick of being accosted by beggars for food and change whilst going about their daily activities??

That was a lot of work to conclude the obvious. Demand outstrips supply!

I guess that is why analysts are paid much less than traders 🙂