AUT’s Briefing Papers initiative has kindly allowed us to syndicate their recent series on housing. The third paper is by University of Auckland economist Ryan Greenaway-McGrevy:

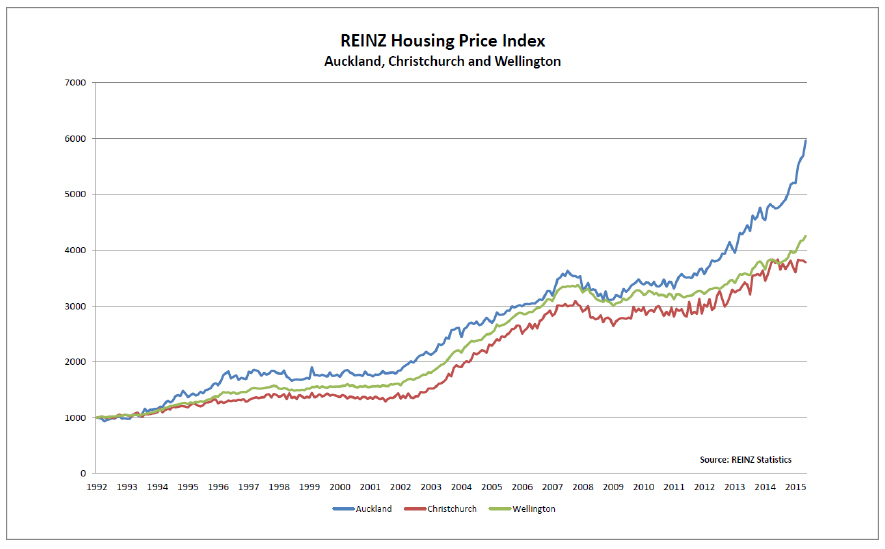

As of May 2015, the average house price in the greater Auckland region was $828,502. In May 2012, it was only $562,454. That is nearly a 50% increase over only three years. Can anything justify this incredible growth in prices, or is it all a bubble?

Peter C.B. Phillips and I address this question in a recent article to appear in New Zealand Economic Papers: Hot Property in New Zealand: Empirical Evidence of Housing Bubbles in the Metropolitan Centres. One of our key conclusions is that there is an ongoing bubble in the Auckland real estate market.

In Hot Property, we try to restore some objectivity to the difficult task of determining whether or not there is a bubble in New Zealand’s real estate markets. But what exactly is an asset bubble, and how can we spot one? A bubble describes a situation in which an asset price is substantially inflated relative to the asset’s fundamental value, which is the present value of expected income from the asset. But while we can easily observe asset prices, it is harder to observe expected fundamentals. Many arguments over the existence of asset bubbles boil down to whether or not high asset prices can be justified by expected incomes. These arguments sometimes persist long after the prices have come crashing down. For example, see this exchange between Eugene Fama and Ivo Welch from 2002 on the famous NASDAQ bubble: http://www.ivo-welch.info/teaching/famaconversation.html. Fama is one of the most frequently-cited financial economists, and is known for the efficient markets hypothesis. Arguments over the existence of bubbles lead to a large experimental literature that has established the existence of asset bubbles in the laboratory setting (see, for example, Smith, Suchanek and Williams, 1988). Outside of the lab, however, it is remains difficult to spot a bubble by focusing only on asset prices, because we never really know what market participants’ expectations are.

It may be more productive to focus on the growth rate in prices, rather than the price level, when trying to spot a bubble. Bubbles occur because sufficient numbers of market participants purchase an asset in anticipation of future price increases. This can generate a self-fulfilling prophecy, in which asset prices spiral upwards simply because market participants think that prices will increase. As more and more buyers enter the market in anticipation of future returns, prices increase, and they increase at an accelerating rate. As I will discuss below in more detail, it is harder to justify this accelerating price growth in terms of changes in expected future income from the asset. We therefore look for accelerating price growth when trying to spot an asset bubble. This general approach to bubble detection was first proposed in the 1980s (See, e.g., Diba and Grossman, 1988).

The statistical bubble detection tests we employ are designed to establish whether prices are growing and at increasing rate. Peter and his other co-authors provide the theory for these statistical methods in a series of papers (Phillips, Shi and Yu, 2015a; 2015b). A key feature of the methods is that acceleration in price growth must occur over a sustained period in order for us to identify it with any acceptable degree of statistical precision: We are not talking about accelerating price growth over a few months, but a few years. The methods provide not only an indicator of whether an asset is currently experiencing a bubble, they also provide date stamping mechanisms for identifying when the bubble begins and ends. In other empirical applications the methods have proved to be very adept at capturing the onset of bubbles in other asset markets, such as stocks and commodities. And importantly, the end of the bubbles always coincides with a fall in the nominal price of the asset in these empirical applications.

Using this method we identify an earlier, broad-based bubble in most of the regional real estate markets of New Zealand. The bubble appears first in Auckland and Wellington in mid- 2003, before spreading to the other main centres. The onset of the bubble suggest that it was part of a broader global bubble in real estate. The bubble burst with the onset of the worldwide recession in 2007, and coincided with about a 10% fall in nominal house prices.

More recently however, the tests show that Auckland once again entered bubble territory in mid 2013. As yet, the bubble in Auckland has not ended, nor has it spread to other parts of the country.

Many readers will disagree with our conclusion and argue that the accelerating price growth in Auckland is entirely justified by the fundamentals. We mitigate these concerns to an extent by normalizing house prices by an indicator of asset income – in the paper we use either rents or incomes – before running our battery of statistical tests. By doing so, we rule out the possibility that asset prices have been growing exponentially because rents and incomes have been growing exponentially. This leaves open the possibility that price growth reflects exponential growth in expected future fundamentals. But while it is easy to generate a fundamentals-based narrative that results in price growth, it is difficult to construct a narrative that can generate accelerating price growth over a prolonged period of time. This is because asset prices incorporate news relatively quickly, and certainly not over a period of several years. Consider, for example, that the Reserve Bank recently cut interest rates and signalled the beginning of monetary easing in the economy. If this cut was a surprise, and all else being equal, this should lead to an increase in house prices, but not an acceleration in house price growth over the next few years. Many of the common rationalizations for high prices in Auckland – such as lower interest rates or high migration rates – fall into this category. An unexpected increase in migration, or an unexpected decrease in mortgage rates, is good news for property owners, and should lead to a relatively quick increase in real estate prices. But in order to generate accelerating price growth over a sustained period, we would need a sequence of good news that persists over several years. No one is that lucky.

Do bubbles always collapse? Nobel Laureate Jean Tirole provided the conditions for a bubble to survive in an economy (Tirole, 1985). These conditions include durability, scarcity, and common beliefs, and housing sure does appear to be scarce right now. Up until this point in time, urban zoning restrictions have tied real estate to land in Auckland: We do not have the same high density planning as many other cities in the world, and so the number of dwellings per unit of land has been more-or-less fixed. Right now, housing is scarce because land is scarce. If this link between land and real estate persists, then we may just be sitting on a rational bubble. Happily however, the current version of the Auckland Unitary Plan allows for a potentially large increase in the number of dwellings within the city limits. If approved, the land restrictions on dwellings will be significantly relaxed, allowing supply to better respond to the price signal.

Where to from here for Auckland? Unfortunately, the empirical bubble detection literature currently offers little in terms of predicting the future. It is apparent, however, that it can be a long time between when the bubble is first diagnosed and when it finally collapses: Periods of five years or longer are not uncommon. It would be foolish for me to make any claims regarding when the best time to buy or sell a house is, or whether prices will increase or decrease next month. But can real estate price growth continue to accelerate indefinitely? I wouldn’t bet the house on it.

References:

Diba, B. and H. Grossman (1988). “Explosive Rational Bubbles in Stock Prices?” American Economic Review 78, pp. 520-30

Greenaway-McGrevy, R., and P.C.B Phillips (2015). Hot Property in New Zealand: Empirical Evidence of Housing Bubbles in the Metropolitan Centres. New Zealand Economic Papers, forthcoming.

Phillips, P. C. B., Shi, S. and J. Yu (2015a). Testing for Multiple Bubbles: Limit Theory of Real Time Detectors, International Economic Review, forthcoming.

Phillips, P. C. B., Shi, S. and J. Yu (2015b). Testing for Multiple Bubbles: Historical Episodes of Exuberance and Collapse in the S&P 500, International Economic Review, forthcoming.

Smith, V. L., Suchanek, G. L., and A.W. Williams. (1988) Bubbles, Crashes and Endogenous Expectations in Experimental Spot Asset Markets. Econometrica 56, 1119-1151.

Tirole, J. (1985). Asset Bubbles and Overlapping Generations Econometrica 53, pp. 1499-1528

Processing...

Processing...

Is there similar movement in the Construction Price Index?

Is the price of building materials moving at a similar rate?

I feel that there is a real problem with our building material costs which no one seems to be addressing!

Not if this is correct (eg p13):

http://www.constructionstrategygroup.org.nz/downloads/BRANZ%20Study%20Report%202013.pdf

I can’t remember what the slightly more recent ProdComm report said, but I think it’s probably similar. Of course, materials are only a small part of overall costs to deliver new housing.

I think most interesting graph is on page 9 which shows the rate of increases in new sections price along with house+land builds, existing house and new sections, over 20+ years from 1992 to 2013.

Over that time, sections went up the most – by a factor of 5 relative to 1992 prices, all other prices only went up by factor of 2-3. So sections in 2013 were worth twice as much in “real” terms now compared to 1992.

Section prices anywhere in Auckland are rapidly increasing and explains a large part of the increase in house prices.

According to graphs later in that report “land costs” including development levies and other costs like infrastructure builds made up 43-45% of a “house+land” package in Auckland in 2013, pretty similar whether its a large or medium sized house.

I think another factor is true replacement costs of existing housing stock closer to town – if you consider a house in the whops costs at least say $600K (in the “affordable range we’re told) for house on say 400m2 of land.

Then the “replacement cost” of a similar sized (but new) house, on an existing, but bigger e.g. 800m, section, much closer to town – is easily worth double that.

People are pricing in the commuter costs to the houses closer to town and bidding up those prices accordingly.

And once you factor in the development potential of these houses with large sections, the opportunity costs of being able to redevelop rather than keeping it as it is become apparent.

Especially if development rules under the Auckland Council will soon allow that 800+m2 section to have two or even three homes on it – and each will be worth at least $100K more than the same size and build quality place out in the whops on a similar 400m2 section (so the closer in ones now go for say $700K+ each) – given their closer proximity to town.

So the price of that “old dunger house near town with a large section” is suddenly worth a lot more than it was a few years back.

Case in point was in todays Herald with some house in Mt Roskill getting $1.8m earlier this month – the reason why so much?

It is a ok house, but comes with a huge 1,400m2 of section – thats able to have 3-4 or even more houses put on it, under the UP, so of course the “house” is worth a lot of money – because the land it is on is being priced for what it can be redeveloped and sold for, not for use as a single house rental unit.

Yes, I believe our construction cost is to the roof. A new house in hobsonvill point now cost 900k to build. With land it will easily cost 1.4 million.

Our material distributor has a huge margin and can continue to do so by exploiting building code compliance and tax policy to block oversea competitors.

Also NZ are slow to adept to factory construction technique such as pre-fab. Most house is still hand built by builders.

Since our construction technique is hand built, builder’s labour price has been driven up due to high demand and low supply.

Finally our council induce a substantial compliance costs and complexity that cost money and time.

A reasonable house can still be built by an owner/occupier for around $3000/m2, and one with non-standard architecture for about $4000/m2. Developers can get this down to more like $2500/m2 or less. Stick with a reasonable size place (100-120m2) and you can easily build it for less than $400k. It is the land that has really gone crazy.

I’ve always liked Lockwood Homes and would rather have had a cheap house with a decent garage/workshop than a massive house on a medium section. Unfortunately current developer persuasions and recent land covenants make this worse than just unaffordable, it’s a style of housing that simply isn’t being built anymore. You have to be happy with a low-stud double garage (and a squeeze at that) and a relatively large house with no free land area or buy something that already exists.

I’m not sure what the answer is, but I suspect giving the council to double-rate land-banked areas of a certain size would increase the amount of land freed up for development, but I’m not sure how you get around covenants. Expensive land also makes commercial & storage space expensive too, so merely keeping projects or toys off-site (essentially TPWing what I’d keep in a garage) becomes impractical too. People insist there are lifestyle concessions to be made with apartment living, but we’re doing a lot of that with the status quo already without realising it.

It is correct in principle.

However a better model is to normalize the rate of increase to interest rate, inflation, population, and current housing supply.

The more I think about it the more I like their definition of a bubble.

You could model changes in house prices in the period from say 2000 to 2008 as a function of various factors (e.g. interest rates, inflation, population, and housing supply) to , and then use those factors to generate a counterfactual house price index for the 2008-2015 period. Finally. you could compare this counterfactual to actual price changes in the same period, as per that graph, and determine whether there was a statistically significant difference.

Simple and intuitive. The only potential problem I see is endogeneity: specifically simultaneous causality between the dependent/independent variables often runs two ways.

I’d caution against anyone – researchers, buyers or sellers treating “The Auckland property market” as one gigantic homogeneous whole entity, in which all parts are of the same value or will experience the same effects (boom or bust or in between) at the same time.

There are it seems many sub-markets each jostling with, and against each other that collectively define the property market, but for which each sub-market has its own set of particulars and underlying fundamental values.

The only thing that they collectively share is that they are all usually within a reasonable commute distance of “jobs in Auckland” for the people that live in those houses. which is why they are relevant to the Auckland housing market. Properties in New Plymouth for instance are simply too far away to be considered relevant for anyone living and working in Auckland so they are not relevant.

The old adage about a rising tide lifts all boats (including the ones with leaks/holes in them), and its only “when the tide goes out” that you can see the difference in stark contrast.

Same with property the rising market is currently lifting all houses in value, it won’t be until the market turns that those houses that are truly closer to the underlying value and which will retain their value will become apparent.

One thing is however, that the authors talk about “sustained good news over many years” is the main thing needed to avoid the obvious explanation of sharply rising prices is a bubble.

In fact we have that in the form of the need, thanks to projections by SNZ and Auckland Council, for Auckland to fit in another 700,000 to 1 million people within its boundaries over the next 30 years, with most projections indicating that means another 400,000 “homes” needed for those future residents over that time. That is a long term, multi-year “good news story”, it can and must be done as a long term managed task because of the sheer scale of the undertaking. You cannot magic that many houses in one place that easily. This is why the PAUP is requiring intensification to occur to “make room” for those 400,000 new homes. No other part of NZ has had to manage that scale of peopulation issue over that period of time in recent memory. Its probably almost nearer to the old Otago Gold Rush days than anything in living memory. It is a good thing to have, but it is a potential disaster for all NZ if not done well.

And this tide of people is therefore providing this massive flood tide of “future demand” that has to be catered for. And when you factor in that Auckland is not currently building enough houses to accommodate the current levels of demand let alone build for the projected levels of growth, and it hasn’t managed to do so for 50+ years, then you realise that the fundamentals of the Auckland market have very likely shifted relative to the rest of NZ housing markets.

This doesn’t mean that the market fundamentals don’t apply, it just means that specific fundamentals are more of an international context and the scale of the “unsustainability” that exists now is perhaps not as high as some are saying.

Yes there is a bubble now, there are many bubbles in Auckland. But how long before they individually or collectively start to implode?

And like those rising boats, which ones are the duds may not become apparent more some time, there will be some sad stories along the way of people who get badly burned, there will be stories of people who do really well, and there will be a lot somewhere in between. It may take several boom and bust cycles before the new fundamentals become well understood and a lot of pain will ensue until that is clear. That pain will be in many forms, beside house prices, it will show up as traffic issues, infrastructure issues, higher rents, higher incomes, longer commutes even whether international companies come to NZ at all.

Its not all bad, but I don’t think even the Government has a proper handle on the scale of the changes afoot nor the wit to understand how to manage it. They simply treat Auckland a big country town, its got way way beyond that. And its got a long way to go.

One thing to keep in mind is that the last couple of years have seen the NZ$ fall fairly substantially.

We sold up in Auckland in late 2013 to move overseas. Whatever additional capital gain we missed out on by selling two years ago and not getting (what?) 20-30% more on the sale price, would be erased by moving NZ$ to the US at 65c not 85c. To the extent that prices in Auckland are a function of cashed-up overseas buyers, this is a part of the story.

Someone from the US with NZ$500K to spend 2 years ago would now have more like NZ$650K at their disposal.

This might (partly) account for inflation in construction costs also.

Of course, none of that stops it from being a bubble either from an international, or more especially, a local perspective.

yes that is a good point and is also something I have also been pondering. If demand is being driven by overseas investment, then a falling NZ dollar would serve to increase the demand for NZ property from overseas. A corollary of this is that reductions in interest rates may serve to increase demand for property in two ways: 1) directly, by way of lower interest rates and 2) indirectly, by way of a lower exchange rate.

My gut feeling is that house prices will drop in the next 2-3 years as 1) lower economic growth (from lower export prices) flows through into weaker net migration and 2) an increase in the supply of new housing in Auckland (which we’ve already started seeing). And if house prices were to drop, then this would allow interest rates to be even lower again? Assuming, of course, that inflation in other sectors doesn’t start to run rampant.

Interesting times. A related question, which is slightly closer to home, is whether I should fix my home loan rate or continue to float :). The latter has been very good for me the last few years, and I still see potential for interest rates to drop further because of issues in China and El Nino etc. But who knows?